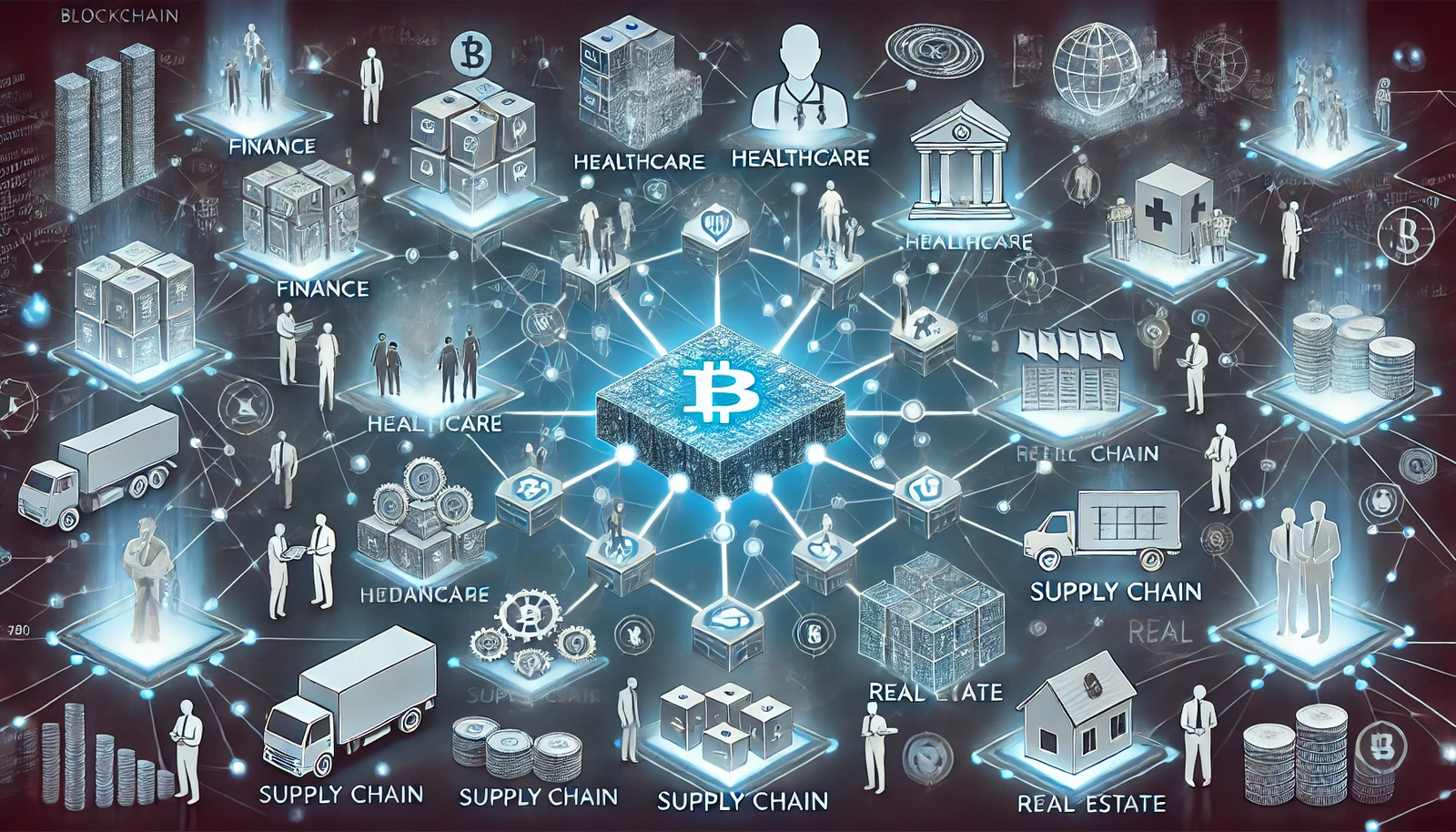

Blockchain technology is revolutionizing multiple industries. Financial transactions that took days on traditional systems can now be completed within seconds using blockchain.

Blockchain provides crucial transparency and traceability in democratic elections, helping prevent vote tampering. Furthermore, this technology enables companies to track products from origin to customers.

Decentralization

Blockchain technology is a revolutionary invention that enables secure and transparent transactions. While its main application may be cryptocurrency transactions, its application spans beyond cryptocurrency into many other industries as it continues to develop over time. As it becomes more mainstream, it promises to transform how business is done – cutting costs, improving data privacy, and creating positive social impacts while remaining hack-proof! Blockchain’s use continues to gain ground.

Though blockchain technology offers numerous advantages, its early stages still present many obstacles that must be addressed. Scalability issues remain particularly difficult and some blockchain systems consume considerable energy when running networks – which has significantly hindered its progress thus far. Solutions are currently being researched to overcome such problems and expedite the growth of this emerging field.

The blockchain system enables parties to transfer assets directly without intermediaries, including money, digital information, and even real estate. Before using this technology for such purposes, one must understand its limitations, such as data transfer limitations, limited security protections, and high energy consumption rates.

However, blockchain may provide more decentralization than can be reached with existing infrastructure alone, providing individuals with a discreet way to exchange value and collaborate in new forms of collaboration. Furthermore, its redistributive effects across global systems enable new patterns of human participation that otherwise would never emerge.

Blockchain’s immutability and transparency make it an effective tool for democratic elections since any attempts at manipulation would be impossible. Furthermore, it provides a secure transactional system without central control or fraud risks; its technology is being adopted for various other uses, such as supply chain management and cybersecurity.

Transparency

Blockchain technology is revolutionizing many industries. Its application in banking and finance is particularly significant. By creating a transparent record of transactions, Blockchain eliminates fraud while adding extra security. Companies using Blockchain can track and verify data while reducing cybersecurity risks; finally, it helps accelerate payment processing times while simultaneously cutting costs.

Blockchains are distributed ledgers that enable individuals and groups to securely record and share data without relying on a central authority for data storage and access. Unlike traditional databases that may be vulnerable to cyber-attacks or have centralized control, blockchains use cryptography to prevent access and tampering – making them ideal for sensitive data such as financial transactions.

Bitcoin is an innovative cryptocurrency that utilizes blockchain to record transactions. This immutable ledger provides an effective method of recording many kinds of information, from elections and product inventories to state IDs and deeds of homes – not to mention being tamper-proof and having many advantages over centralized systems.

Blockchain technology can assist businesses in creating more transparent supply chains, essential for regulatory compliance and customer satisfaction. Furthermore, this technology can increase transparency in public procurement processes while decreasing corruption; Colombia and Peru have already begun using it for auditing procurement procedures, while future uses could include monitoring electoral processes more transparently.

Although blockchain is innovative, it has yet to reach its full potential. Still in its infancy and with a high failure rate, blockchain may offer an effective solution to companies that need to connect their supply chains to central databases.

Blockchain will have multiple uses in the future. For instance, it could help track insider trading sources, goods movement tracking, or medical record storage – and, more importantly, help financial institutions increase transparency through streamlining business operations.

Immutability

Security and transparency are becoming paramount concerns with industries relying heavily on digital datas. Blockchain technology’s immutability of records provides an essential pillar of trust for digital transactions and information sharing; however, this feature may be vulnerable to attacks by malicious actors; therefore, systems must be implemented to counter malicious activities and ensure the immutability of blockchain records is not compromised.

Blockchain’s immutability relies on cryptographic algorithms, making altering data impossible once it enters the system. Each block of transaction data generates its own hash value; comparing hash values across networks makes it easy to detect any changes to this data. Furthermore, its design makes it highly resilient and decentralized, meaning it will function even if some participants or nodes become unavailable.

Blockchain’s immutability enables it to track the origin and authenticity of goods and services, providing businesses more transparency while decreasing fraud and counterfeiting risks. Furthermore, using this immutability can reduce costs by eliminating intermediaries and automating processes, making cross-border transactions quicker by lowering fees and delays.

Blockchain has many uses in finance, healthcare and insurance – from tracking patient medical records securely through platforms like MedicalChain to helping providers access it quickly.

Blockchain technology is increasingly being implemented in the insurance sector to record and validate claims quickly and fairly, speeding up processing while guaranteeing fairness. Furthermore, smart contracts based on blockchain can automate settlement procedures to further lower costs and simplify operations within this industry.

Technology is also employed to manage intellectual property in the digital media industry, helping prevent piracy by guaranteeing only one true copy of each file. Furthermore, creators’ rights are protected by only authorizing recipients to receive copies of their works.

Security

Blockchain has long been associated with cryptocurrency, yet its applications go beyond this industry alone. Offering transparency, immutability, and traceability across a distributed network makes Blockchain ideal for use cases that would otherwise require traditional infrastructures to support.

Blockchain security relies on cryptography and hashing algorithms, protecting against malicious actors tampering with information and altering subsequent blocks. Furthermore, data stored on a blockchain cannot be removed without altering subsequent blocks; moreover, it’s stored across a peer-to-peer network rather than being stored centrally, reducing risk from single-point failures; furthermore, it uses consensus algorithms such as proof of work (PoW) or proof of stake (PoS) which verify the authenticity of the information in various ways; proofs used within blockchains are two such mechanisms used within these mechanisms for verification; other popular mechanisms include proofs of work (PoW) or proofs used within it a blockchains.

Blockchain offers businesses another benefit by allowing direct transactions between parties without intermediaries like brokers or bankers, saving both time and money while helping prevent fraud by recording each transaction and its participants, guaranteeing only eligible parties receive funds.

Blockchain is being leveraged within the financial industry to speed up fund transfer times, significantly decreasing bank processing delays by up to one week compared with older methods and making processes more efficient for both parties involved.

Blockchain’s use in financial services is only the tip of the iceberg; other industries are quickly adopting its technology, including healthcare, transportation, and real estate. Blockchains can assist healthcare practitioners by tracking patient records; these systems can even track medication adherence and help prevent medical mistakes – genome sequencing startups have even adopted its use!

Blockchains can be used to create secure digital IDs that enable people to manage and share their data securely with others. Blockchains can also be used to monitor supply chains and offer transparency for all stakeholders involved – this encourages companies to improve their practices and identify inefficiencies while enhancing customer experiences and cutting down costs by eliminating intermediaries and making business more cost-effective and efficient.